If 'We' Get Divorced, Can I Keep the Company and the Money? | Detailed Explanation of Company Share Issues under the Civil Code's Marriage and Family Section

A detailed breakdown of how company equity, capital contributions, and business income are classified and divided in divorce under Chinese civil law, covering pre-marital and post-marital entrepreneurship scenarios.

Recently, a variety show became wildly popular, and many hot memes spread across the internet.

This included the following:

In today’s society, starting a business is an important way for many people to accumulate wealth and achieve class mobility. However, when a marriage comes to an end, the division of company equity often becomes one of the most complex issues in divorce disputes.

This article will explore in detail how company shares, income, and other assets are identified and distributed during a divorce from different perspectives.

Providing some ideas for all the bosses and future bosses out there.

This article represents only the author’s personal views and does not constitute legal advice or legal opinion.

I. Basic Legal Framework

The following legal provisions are relevant to the handling of company property in divorce cases:

Civil Code:

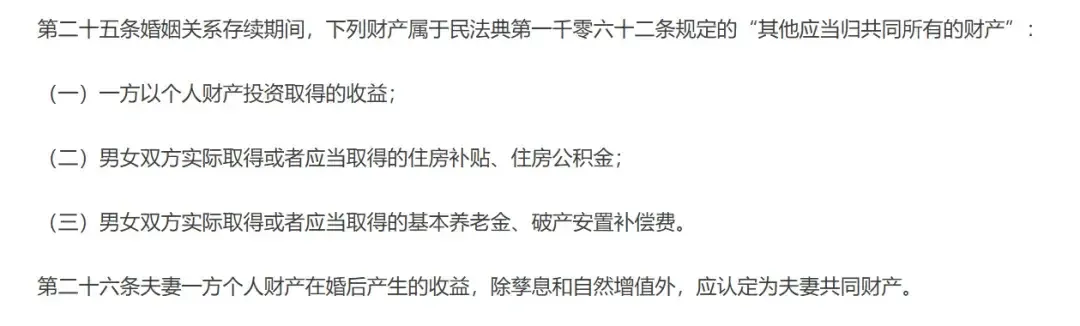

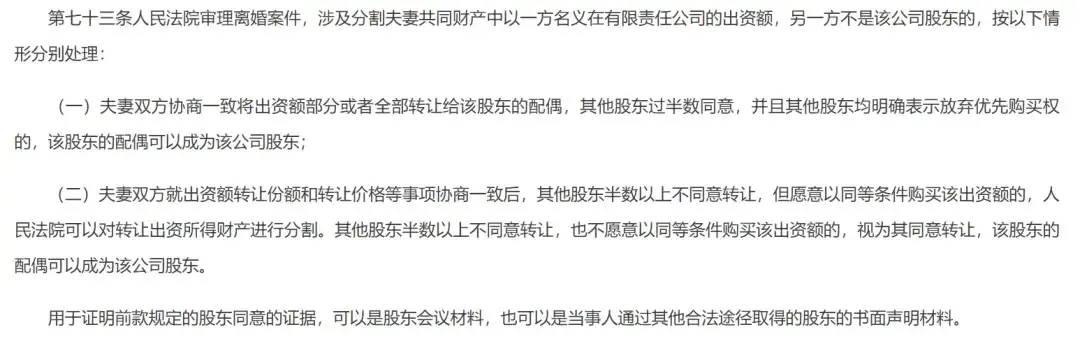

Article 1062: The following property acquired by the spouses during the period of marriage is jointly owned by the spouses: (1) Wages, bonuses, and labor remuneration; (2) Income from production, operation, and investment; (3) Income from intellectual property rights; (4) Property inherited or gifted, except as provided in Article 1063, item (3); (5) Other property that should be jointly owned. Spouses have equal rights to manage jointly owned property. Article 1063: The following property is the personal property of one spouse: (1) Pre-marital property of one spouse; (2) Compensation or damages received by one spouse for personal injury; (3) Property specified in a will or gift contract as belonging only to one spouse; (4) Daily necessities exclusively for one spouse’s use; (5) Other property that should belong to one spouse. Article 1087: Upon divorce, jointly owned property shall be handled by agreement between the parties; if no agreement is reached, the people’s court shall make a judgment based on the specific circumstances of the property, following the principle of protecting the interests of children, the wife, and the no-fault party.

Supreme People’s Court’s Interpretation (I) on the Application of the Civil Code’s Marriage and Family Section:

However, actual situations vary greatly. The following sections will discuss different scenarios separately.

Note:

1. The discussion in Part 2 assumes that the parties have not signed any agreement regarding property matters.

2. Excludes sole proprietorship issues (as game companies basically have no possibility of this form).

II. Equity Attribution and Division Under Different Scenarios

Pre-marital Sole Entrepreneurship

For a company founded by one spouse before marriage, the equity in principle belongs to the pre-marital personal property. Even if the company develops well after marriage and generates considerable income, ownership of the equity itself still belongs to the founding spouse.

However, income generated by the company during the marriage, including profit distributions, is jointly owned property. That is, although the spouse cannot claim ownership of the company, they have equal rights to claim a share of the income generated during the marriage.

In fact, regardless of the scenario, except when both parties are registered shareholders and income is distributed according to the registered ratio, the company’s post-marriage income must be distributed to the other spouse. Therefore, this point will not be repeated below.

Division Plan:

In this case, the other spouse has no right to demand a division of company equity but is entitled to claim half of the undistributed profits generated during the marriage.

Specific methods include:

- Conducting a special audit of undistributed profits to determine the amount generated during the marriage;

- The shareholder spouse can achieve division through profit extraction, cash compensation from personal funds, or replacement with other equivalent assets;

- If both parties and other shareholders (if any) agree (requires majority approval, same below), division may also be achieved by converting profits into increased capital and then distributing shares, enabling the other spouse to obtain corresponding equity.

Pre-marital Company with Post-marital Capital Increase Using Joint Property

If one spouse founded a company before marriage but used joint property after marriage to increase capital, it is necessary to distinguish between the original equity and the newly added equity.

The original equity remains pre-marital personal property. However, the newly added equity formed by the capital increase using joint property should be recognized as jointly owned property. Even if the spouse was not added to the shareholder register at the time of the capital increase, the value of the newly added equity must still be divided according to the contribution ratio upon divorce.

Division Plan:

- The original equity portion still belongs to the individual;

- For the newly added equity portion, if the capital increase funds came from joint property, the newly added equity should be recognized as jointly owned property. The equity share due to the other spouse should be determined based on the valuation ratio before and after the capital increase.

- Division can be achieved through equity transfer, cash compensation, or replacement with other assets.

Post-marital Entrepreneurship Using Pre-marital Personal Property (Registered in One Spouse’s Name)

If a company is established during the marriage but the capital contribution comes entirely from one spouse’s pre-marital personal property and is registered in that spouse’s name, additional evidentiary work may be required when division is needed.

Although the company was established after marriage, if the source of capital contribution can be traced and it is determined that the funds all came from that spouse’s personal property, the equity may still be recognized as personal property.

However, this recognition requires sufficiently strong evidence that the capital contribution indeed came from pre-marital personal property and that no post-marital joint property was mixed in during the contribution process.

Division Plan:

- If it can be sufficiently proven that the capital contribution came from pre-marital personal property, the equity itself can be recognized as personal property;

- However, the other spouse can still claim undistributed profits from the marriage period (refer to the first scenario);

- A sufficiently detailed and credible complete chain of evidence proving the source of funds is required; otherwise, it may be presumed to be joint property.

Post-marital Entrepreneurship with Mixed Capital Contribution (Registered in One Spouse’s Name)

Compared to relying entirely on personal property, a more common scenario is that the company established after marriage used a mix of pre-marital personal property (personal savings) and post-marital joint property (post-marital income, spouse’s savings, etc.). In this case, even if the company is registered in one spouse’s name, the nature of the equity must be determined based on the source of capital contribution.

The equity portion corresponding to the pre-marital personal property contribution can be recognized as personal property, while the equity portion corresponding to the post-marital joint property contribution should be recognized as jointly owned property. In practice, this situation often requires a detailed tracing of the capital source chain to determine the nature of each portion.

Division Plan:

- A special audit is needed to determine the specific proportion of different funds (personal/mixed);

- The equity share to be divided should be determined according to the capital contribution ratio;

- Division can be achieved through one of the following methods:

- With the consent of other shareholders, transfer the corresponding share directly to the other spouse through equity change;

- Compensate or replace with cash or other equivalent assets.

Post-marital Entrepreneurship Solely with Joint Property (Registered in One Spouse’s Name)

For a company established after marriage using joint property, even if registered in one spouse’s name, the equity should be recognized as jointly owned property. In this case, it cannot be considered personal property simply because the business registration is in one spouse’s name. Upon divorce, the other spouse has the right to claim equal division of the company equity.

However, it should be noted that when there are shareholders beyond just the couple, the preemptive rights of other shareholders must be considered during division. When the only actual shareholders are the couple and neither is willing to co-manage the business with the other, considering the continuity and stability of the company’s operations, courts handling such disputes may tend to let the actual operating spouse retain the equity and compensate the other spouse through other means.

Division Plan:

- In principle, the other spouse is entitled to half of the equity;

- Considering the continuity of company operations, the following methods can be adopted:

- The actual operating spouse retains all equity and provides equivalent compensation to the other spouse;

- To ensure normal operations, negotiate a reasonable installment payment plan;

- Achieve a balance of interests through replacement with other assets.

Post-marital Joint Entrepreneurship with Company Registered in Both Names

This is the clearest scenario!

In this case, the attribution of equity is directly determined according to the shareholding ratio in the business registration, making it clearly defined proportional property. Upon divorce, the parties can directly divide or negotiate the disposal of shares according to the registered shareholding ratio.

Division Plan:

- Division can be conducted directly based on the registered shareholding ratio (note: not a default 50-50 split). The parties can negotiate for one party to buy out the other’s shares entirely or partially, with compensation in cash or other equivalent assets;

- If both parties are willing to continue holding shares, the status quo can be maintained.

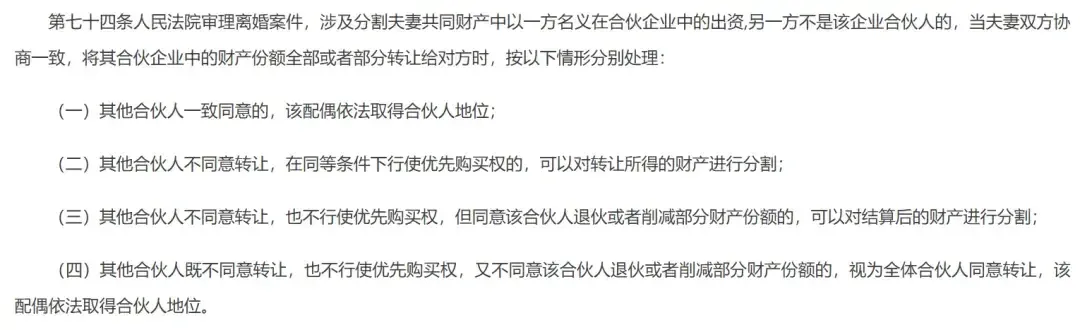

Special Situations in Partnerships

Partnerships differ in nature from companies, especially general partnerships, where the core lies in the trust relationship among partners, i.e., “people-centric.”

Handling Principles:

-

If it is a general partnership:

- Without unanimous consent from other partners, the spouse cannot directly become a partner due to divorce division. However, other partners should exercise their preemptive rights;

- If preemptive rights are not exercised, other partners must agree to the partner’s withdrawal or reduction of their share;

- The divorcing couple divides the proceeds from the purchase of the share or the capital returned upon withdrawal;

- If other partners neither exercise preemptive rights nor agree to withdrawal or reduction of the share, the spouse automatically becomes a partner.

-

If it is a limited partnership, the handling of the general partner’s share follows the rules for general partnerships; the limited partner’s share can be treated similarly to company equity.

III. Special Factors to Consider During Division

When handling company equity division, it’s not simply “split and done.” Multiple important factors must be fully considered to avoid adverse effects on individuals or the company.

Company Equity/Governance Structure

In some companies, especially those with multiple shareholders, family businesses, or companies with many investors, equity division may affect the control structure.

If the original shareholder’s shareholding is close to a control threshold (33.4% / 50% / 66.7%), division could lead to loss of control or a deadlock, significantly impacting normal company operations.

Therefore, when designing a division plan, priority should be given to retaining company shares and avoiding equity being purchased by other shareholders. If equity is successfully divided, consider maintaining control stability through voting rights delegation, unanimous action agreements, etc., with the former spouse.

Also, consider whether the equity division would trigger conditions for changes in decision-making mechanisms of corporate governance bodies such as the shareholders’ meeting or board of directors, to avoid losing decision-making power in the company or even being ousted by the shareholders’ meeting or board of directors.

Development Stage and Operating Conditions

If the company is in a rapid development phase, undergoing major investments, or planning for an IPO, equity division may affect the company’s financing plans or IPO process.

Some investors may value equity clarity and company structure stability. If shareholder marital issues cause company instability, or if the former spouse obtains company equity and even triggers a “power struggle,” the company may lose potential financing opportunities.

In this case, prioritizing the retention of shares is still recommended. When cash flow is insufficient to retain shares, consider methods such as installment payments or setting equity repurchase clauses to meet division needs as much as possible without affecting the company’s development plans.

Company’s Debt Situation

Some companies appear to have considerable equity value on the surface but actually carry substantial debt, or may even be in a loss-making state. In such cases, simply valuing and dividing based on registered capital or net book assets could lead to severely imbalanced outcomes, with “income” going to the former spouse and debts remaining with oneself.

“Parting as lovers” still shouldn’t mean leaving yourself with all the hardships.

Therefore, before conducting equity division, it is advisable to conduct a comprehensive audit of the company’s assets and liabilities, paying special attention to contingent liabilities, external guarantees, and other hidden risks, to ensure that the division plan is based on the true financial condition.

IV. Practical Suggestions

Based on the above analysis, to avoid various post-marital complications, some preventive measures can be taken in practice.

Note: “Prevention” does not mean “lack of love” — it is merely preparatory work to clarify issues and avoid future disputes.

At the early stage of starting a business, it is advisable to keep clear records of the source of capital contributions and retain relevant vouchers.

During the marriage, care should be taken to maintain a clear distinction between personal property and joint property, and to retain complete written records of important equity transactions.

If necessary, consider engaging a third party to formulate a prenuptial/postnuptial property agreement based on the actual circumstances, signed by both parties.

When entering the divorce negotiation phase, it is advisable to engage a professional third party to evaluate the equity value, fully consider debt issues, taxes, etc., design a reasonable division plan, and maintain good communication with other shareholders to seek their understanding and support.

V. Final Thoughts

In practice, when encountering situations where company equity needs to be divided due to divorce, various thorny issues often arise. After all, equity issues not only affect the vital interests of the couple but may also impact the company’s daily operations and the rights of other shareholders. When dealing with such issues, it is necessary to strictly follow legal provisions while fully considering the actual circumstances to balance the interests of all parties.

Ultimately, the root cause is the lack of prior agreements.

It is recommended that couples who are planning to start a business or have already started one should prepare in advance through reasonable institutional arrangements and signed agreements, preventing problems before they occur and avoiding future disputes.

Finally, and most importantly:

Do I deserve a like?

If you could also follow, share, and click “在看,” that would be even more wonderful.